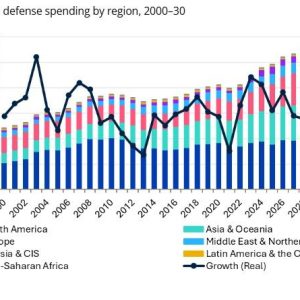

Europe’s rearmament is accelerating. NATO’s latest dataset for NATO 2025 defence expenditure confirms sharp real‑term growth across European Allies, while the United States remains the Alliance’s anchor by absolute outlays. Beyond topline numbers, the new figures signal where capability will materialise over the next five years—and where gaps will persist. [1]

Europe surges; the US still anchors the ledger

The headline story in NATO 2025 defence expenditure is momentum in Europe and sustained American dominance. NATO’s official compilation—built on Allied defence ministry returns and harmonised macro inputs from the European Commission, IMF, and OECD—shows double‑digit growth across much of Europe. Germany’s defence budget is estimated at $93.7 billion, edging past the UK at $90.5 billion, while France stands at $ 66.5 billion. Italy ($48.8B), Poland ($44.3B), Canada ($43.9B), Spain ($35.7B), Türkiye ($32.6B), and the Netherlands ($28.1B) follow. [1]

The United States remains decisive at $980B—more than ten times the next European spender. That scale underwrites global mobility, nuclear deterrence, ISR, and munitions stockpiles that the Alliance relies on for deterrence and reinforcement. But the new pattern is clear: European treasuries are moving, and procurement pipelines will follow.

Burden‑sharing by GDP: the eastern flank leads

Measuring commitment by GDP share rather than absolute dollars flips the leaderboard. Poland tops NATO at 4.48% of its GDP, followed by Lithuania (4.00%), Latvia (3.73%), Estonia (3.38%), and the Nordic countries (Norway, 3.35%; Denmark, 3.22%). The United Kingdom sits at 2.4%, and France at 2.05%, on NATO’s definition. [1]

This regional pattern reflects geography and threat perception. Front‑line Allies are prioritising ground‑based air defence, deep fires, stocks of 155mm ammunition, and counter‑UAS suites. Northern Allies are simultaneously investing in maritime domain awareness and air policing on the High North—areas where pooling with the UK and US yields immediate returns.

The UK trajectory: steady real‑term growth, uneven force outcomes

On NATO’s constant‑price series (2021 USD), the UK rose from $62.7B in 2014 to an estimated $81.3B in 2025, with a brief dip in 2015 and a small retracement in 2023. That equates to +29.6% in real terms over the period. [1]

What does that buy? The answer depends on the balance across the nuclear enterprise, carriers and escorts, land fires, and munitions depth. The Strategic Defence Review 2025 sets an intent to reach 2.5% of GDP by 2027 and aims for 3% in the next Parliament, contingent on fiscal conditions—signals that will shape the Army’s artillery recapitalisation, A2/AD enablers at sea, and sovereign missile supply chains. [4]

“Increased funding must translate into actual military capabilities—readiness and strength, not just financial commitments.” — Secretary‑General (reports, August 2025). [3]

What the new NATO framework changes

At the 2025 Hague Summit, Allies endorsed a 5% of GDP investment concept by 2035 covering core defence and enabling security functions. In parallel, major reporting has highlighted a 3.5% of GDP benchmark for defence proper; only Poland, Lithuania, and Latvia are already there or above. This reframes “2%” as a floor, not a finish line, and will push choices on industrial base expansion, stockpile recovery, and air‑and‑missile defence architectures. [2][3]

For industry, that means predictable multi‑year demand: 155mm and 120mm lines running at capacity; RAM/SHORAD batteries paired with counter‑UAS modules; and longer‑lead naval programmes insulated by sustained appropriations rather than stop‑start cycles. For treasuries, it means managing defence inflation, FX swings, and workforce constraints to convert inputs into deployable brigades, ready squadrons, and credible magazine depth.

Methodology & caveats (why NATO’s numbers differ from national budgets)

NATO applies a standardised definition of defence expenditure that includes pensions and excludes civil defence and war‑damage payments. It reports in both current prices and constant 2021 dollars for real‑terms tracking. Figures for 2024–2025 remain estimates with a data cut‑off of 3 June 2025, and they may diverge from national statements that use different scopes or deflators. Always check which series you are reading before concluding. [1][5]

Implications to watch in 2025–2028

- Air & missile defence build‑outs. Expect additional Patriot, SAMP/T, IRIS‑T SLM, and NASAMS orders, with C‑UAS layered from soft‑kill to hard‑kill. Our technical explainer on modular radar arrays shows one vector for cost‑effective coverage. [6]

- Munitions sustainment over platform counts. Eastern Allies will keep prioritising artillery and GMLRS stocks; Western Allies must close the depth gap.

- Naval recapitalisation vs. affordability. Carrier and SSN bills compress land‑force headroom; transparent trade‑offs will matter for voters and deterrence credibility.

- Industrial workforce. Hiring and skilling bottlenecks risk schedule slippage even if budgets rise on paper.

Bottom line

The NATO 2025 defence expenditure rollout confirms that Europe has moved from rhetoric to resources. The US still anchors the Alliance, but the growth story is increasingly continental. The policy test now is simple: convert rising inputs into ready units, modern magazines, and credible integrated air‑and‑missile defence. Dollars and percentages are the start—not the outcome.

—

Internal link

For a technology lens on how budgets translate into capability, see our analysis of modular radar arrays for cost‑effective missile defence coverage. Read the analysis. [6]

External link (primary source)

NATO’s official statistical release and full PDF dataset provide the authoritative baseline used in this article. Open NATO’s 2025 defence expenditure release. [1]

References

- NATO — Defence Expenditure of NATO Countries (2014–2025). Cut‑off 3 June 2025; estimates for 2024–2025.

- NATO — Defence expenditures and NATO’s 5% commitment (2025).

- Topic explainer: https://www.nato.int/cps/en/natohq/topics_49198.htm

- Reuters — All NATO members hit old spending target; only three meet new goal (27 Aug 2025); AP coverage.

- UK Government — Strategic Defence Review 2025: Making Britain Safer (policy intent on 2.5% by 2027).

- NATO — Defence Expenditure methodology (constant‑price series; scope differences) — 2024 reference.

- Defence Agenda — Caplink array boosts missile defence (internal technical analysis).

Further Reading

- SIPRI — NATO’s new spending target: challenges and risks (2025).

- UK House of Commons Library — UK defence spending (briefing).

- Research briefing: https://commonslibrary.parliament.uk/research-briefings/cbp-8175/