Russia’s invasion of Ukraine forced capitals to rediscover an unfashionable truth: production is deterrence. The immediate lesson for policymakers is that defence industrial base readiness—from stockpiles to surge capacity and workforce—is now a strategic variable, not a back‑office concern [1]. In a world of rapid, cheap battlefield innovation, nations that can refresh sensors, munitions and software in weeks—not years—shape escalation dynamics and bend the cost curve.

Key Facts

The wargames indicate that long‑range precision munitions can be exhausted within days unless stockpiles and production lines scale [5].

Policy is catching up: the United States released the National Defense Industrial Strategy; the EU launched the European Defence Industrial Strategy [9] [3].

Supply‑chain choke points persist. China dominates processing of key critical minerals used across defence manufacturing [6].

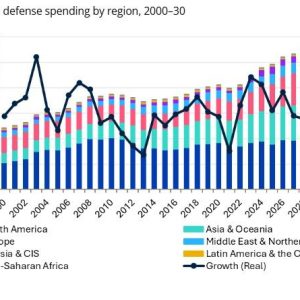

NATO spending is up sharply; nevertheless, capacity and coordination gaps remain [2].

Why industrial capacity is strategy

Artillery shells, precision weapons, drones, and air‑defence interceptors are burned at rates that dwarf peacetime forecasts. Consequently, defence industrial base readiness must be aligned to prolonged, high‑intensity conflict. The CSIS analysis calls for robust stockpiles, warm lines, and deep supply‑chain visibility down to sub‑tiers where single‑point failures often hide [1].

Markets reward efficiency, not redundancy. However, wartime resilience depends on spare tooling, second sources, and pre‑qualified alternatives. You cannot surge a machine‑tool sector or a skilled workforce overnight; therefore, capacity has to be built and kept warm in peacetime.

“Production is deterrence.” Building capacity before crises lowers escalation risk and shortens war.

Munitions math: stockpile first, then surge

Repeated wargames—especially around a Taiwan scenario—show the United States could burn through long‑range precision munitions in a week, outpacing current industrial capacity [5]. Europe faces similar shortfalls despite recent capacity additions. The implication is straightforward: fund munitions as programmes of enduring record, not episodic supplementals; pre‑buy critical inputs; and contract for multi‑year volume with options to accelerate.

Practically, that means target lines for propellants, rocket motors, seekers and energetics; guaranteed orders to de‑risk supplier investments; and shared NATO buffers for items with common interfaces. This is the backbone of defence industrial base readiness.

Open systems and the 90‑day refresh

Ukraine and Russia have demonstrated a continuous innovation loop—drones, ISR, and EW packages evolve on weekly cycles. Acquisition must adapt: open‑systems architectures, modular software, and rapid A/B testing at the edge. Instead of waiting for exquisite upgrades, field spiral increments with clear rollback paths and cyber‑hardening baked in [1].

Allies, co‑production and the capacity web

Industrial superiority is now a team sport. Coproduction agreements, tooling swaps and shared certification standards raise collective output and reduce lead times. NATO’s spending surge since 2022 provides budgetary cover; the task is converting euros and dollars into forgings, guidance sections and launch cells at scale [2]. The EU’s EDIS aims to push this further by tackling fragmentation and incentivising cross‑border orders and interoperability [3].

For programme planners, co‑production is not just diplomacy; it is risk management. Shared stockpiles and interchangeable subcomponents mean partners can backfill each other when factories go dark or shipping lanes are contested. This is core to defence industrial base readiness.

Supply‑chain realities: minerals, machine tools, shipyards

Strategic materials sit upstream of every missile, radar and airframe. China’s dominance in processing rare earths, lithium and cobalt magnifies risk exposure and complicates sanctions calculus. IEA data shows refining is highly concentrated, with China responsible for the vast majority of REE and major shares of lithium and cobalt processing [6].

Downstream, dual‑use sectors like commercial shipbuilding reveal scale imbalances that translate into defence overmatch. Analysts warn China’s industrial base now outproduces Western counterparts by an order of magnitude in key yards—capacity that can ripple into naval sustainment and auxiliary fleets [7].

Policy levers that actually move metal

Lock in demand. Use multi‑year procurement and framework agreements with surge clauses to underwrite supplier capex. Tie payments to throughput milestones and quality yields.

Fund the sub‑tiers. Map bills of material to the tenth tier. Identify single‑point failures and co‑finance duplication where the market will not. Energy‑intensive inputs—powders, energetics, advanced alloys—deserve priority.

Workforce is a weapon system. Expand apprenticeships and certify cross‑skilling pathways. A skilled operator on a five‑axis mill is as scarce—and valuable—as a pilot.

Mandate open systems. Require modular hardware/software interfaces to support 90‑day increments and vendor competition. This keeps the innovation flywheel spinning on the front line [1].

Allied buffers. Establish shared munitions parks and reciprocal priority‑rated orders. Use NATO agencies and EU instruments to synchronise orders and avoid price spikes [2] [3].

What this means for programmes now

Programme managers should audit their top three cost and time drivers and ask a brutal question: “What would it take to triple output in 12 months?” Answers typically include second tooling sets, alternate powders, and supplier financing. That is the practical heart of defence industrial base readiness.

For readers following autonomy and swarming programmes, see our analysis on the UK’s plan to field AI‑enabled drone swarms—an example of where modularity and fast refresh will define advantage. Read the related analysis.

References

- CSIS, “Industrial Roadblocks: Producing at Scale and Adopting New Technologies,” September 16, 2025. Link

- NATO, “Defence Expenditure of NATO Countries (2014–2024),” June 2024. PDF

- European Commission, “First‑ever European Defence Industrial Strategy,” March 5, 2024. Link

- DoD, “National Defense Industrial Strategy — Implementation Plan,” July 3, 2024. PDF

- CSIS, “The U.S. Industrial Base Is Not Prepared for a Possible Conflict with China,” February 22, 2023. Link

- IEA, “Energy Technology Perspectives 2023 — Clean‑energy supply chains vulnerabilities,” 2023. Link

- CSIS, “China Dominates the Shipbuilding Industry,” March 25, 2025. Link

- European Parliamentary Research Service, “European Defence Industrial Strategy,” Briefing, September 2024. Link

- U.S. DoD, “National Defense Industrial Strategy (NDIS) — 2023,” background and PDF. PDF

Internal Link: UK to field AI drone swarms within five years — analysis

External Link: CSIS — Industrial Roadblocks